Mortgage Advice

Our Blog

Follow us on IG

Need A Mortgage

Get pre-approved today! Novus Home Mortgage, a division of Ixonia Bank, offers the most diverse set of loan products in the industry. No matter what situation you may face, we set you up for one thing: to help a family get into a home. Novus Home Mortgage has the product mix for every customer

Buying a home is an exciting time for future home owners. There’s a lot of buzz surrounding the home buying process, which can unfortunately come with a bit of stress. Knowing what to look for can alleviate that stress and set you up for success.

Here’s three tips to consider before committing to a property…

Understand the costs

The most important thing you can do to set yourself up for success in buying a home is to get pre-approved. Getting pre-approved will give you a clear understanding of how much of a home you can afford based on the payment that fits within your budget.

Speaking with a lender will also help you understand other costs outside of a mortgage, such as the cost of taxes and insurance. Does the home have an HOA payment? All of this will need to be considered and fit into your budget.

Another factor to consider is future maintenance costs. If a home is in need of repairs, that should be factored into your budget as well. You should also consider cost of utilities for the home. Luckily, many homebuyers are able to obtain reports on previous utility costs so they have a good estimate.

Research the area

Researching a location and area is all about your lifestyle and your preferences. One of the most important considerations is where the property is in relation to work and school. Would you prefer a short commute? Can you easily pick children up after school on the ways home? Is it close to public transportation, if needed?

Once you have that nailed down, you’ll want to consider the dynamics of the neighborhood. Is a family-friendly neighborhood important to you? What about having shopping nearby. There is no wrong answer, it is completely based on your preference! With nearby shopping tends to come heavier traffic. But that also comes with convenience.

And lastly, always check safety reports. Many local government provide reporting on the frequency and type of crimes committed within their jurisdiction.

Inspect all aspects of the property

Home Inspection

In most cases, inspecting a property comes after an offer has been made, but before closing on the home. In that window of time in-between, you’ll want to look at a few crucial elements before signing off.

The first, and most obvious, is to have a property inspection done by a professional. A professional inspector will check everything on the homes exterior and interior. On the outside this includes examining the walls, foundation, roof, and drainage. On the inside, they will check the plumbing system, electrical system, HVAC, appliances, and so forth.

In some cases, it would also be beneficial to have a pest inspection completed. This will check for harmful pests such as terminates that could cause damage to your property.

Title Search

A title search will need to be done on the property before closing to ensure there are no liens or disputes over the property’s ownership. You’ll also have the option to purchase title insurance which protects you against future instances of fraud. We recommend having a discussion with a title attorney to see if this is a good option for you.

Proper Permitting

Another thing to check for is to make sure that all renovations and repairs were done properly and received the proper permitting beforehand. You don’t want to be stuck dealing with the previous owner’s lazy management.

Plenty of people are still moving these days. And if you’re thinking of making a move yourself, you may be considering the inventory and affordability challenges in the housing market and wondering what you can do to help offset those. A new report from Gravy Analytics provides insight into where people are searching for homes and what they’re prioritizing most right now. That information could help you plan your own move.

1. People Are Moving to Cities with Lower Housing Costs

One big factor motivating where buyers are going is affordability and that’s no big surprise. People are relocating to areas that have less expensive housing options. As a result, small cities are thriving. Hannah Jones, Economics Data Analyst at Realtor.com, summarizes why:

“Affordability is still very much front and center . . . a lot of what’s available is outside of the price range of many buyers. . . . so they look elsewhere for a little more bang for the buck.”

The takeaway for you? If you’re having trouble finding a home that fits your budget, it may help to browse other, more affordable locations nearby.

2. People Want to Live Where They Vacation

And, if you’re already expanding your search radius, you may be able to include a location that features your favorite type of destination, like a suburb near the beach or a mountain town. Data shows many other homeowners are making that type of move a priority today. According to the same report from Gravy Analytics:

“Whether it’s the opportunity to enjoy more weekend hikes in the mountains or to wake up to a lakeside sunrise, people are moving to areas that were once thought of as vacation spots.”

Even with today’s home prices and mortgage rates, here’s why a move like this could be possible for you. If you’re already a homeowner, the equity you’ll get when you sell your current house can help fuel that move and give you the down payment you’d need for your dream home.

3. People Who Work Remotely Are Taking Advantage of that Flexibility

Ongoing remote work is another major factor in where people are moving. A recent report from the McKinsey Global Institute says this about recent movement patterns:

“Many of these moves happened because employees untethered from their daily commutes began to care less about how far they lived from the office.”

If you’re a remote or hybrid worker, you don’t have to live in the same city, or sometimes even the same state, as your job. That means you can prioritize other things, like being closer to loved ones, when buying a home.

In fact, the same McKinsey Global Institute report notes for people who moved during the pandemic, 55% reported moving farther from the office. And since remote work is still a popular choice today, homebuyers will likely continue to take advantage of that flexibility.

Bottom Line

Lots of people are still moving today. If you want help navigating today’s inventory or affordability challenges, and expert advice to help you find your ideal home, let's connect.

Each year thousands of Florida vacationers take advantage of the weather, beach, and endless things to do. At the same time, vacation rental property owners are cashing in on the thriving tourism.

Owning vacation rental property in a high tourism area, such as Florida, is a major way to build wealth. For those considering stepping into owning vacation rental property, here’s a few things to consider.

Advantages

Long or short term

When buying property as a rental, homeowners have the option to choose long term or short term rentals. Both have pros and cons, but both are a great way to have your mortgage paid by someone else, and receive passive income.

Short term rentals are those geared towards tourists and vacationers. Typically, the property will be rented for a weekend or a week. The major advantage of this is more money is typically charged on a per night basis.

Long term rentals, such as 6 or 12 month leases, are typically geared towards locals or those who are moving to the area. The advantage of this is that your income coming in from the property is more predictable.

Florida also has an additional demand that is unique to our market, and that is “snowbird” or winter rentals. With these type of rentals, a person will rent a condo or house for 1 to 3 months during the winter season.

Building wealth

Buying investment property with the intent to rent out is a great way to build your net worth. Both long term rentals and short term rentals have pros

Your own vacation destination

Another major advantage to owning your own vacation rental property is that you and your family can vacation there whenever you want! Instead of paying money to stay at another’s property, you can visit your property that others are paying for.

Financing

When looking to finance your vacation rental property, your lender will factor in a few metrics unique to investment property management.

Debt Service Coverage Ratio

Lenders will take into account how much income the property is likely to produce. This is factored into your overall debt-to-income ratio, which we will cover below. The debt service coverage ratio measures how much rental income remains after paying for all costs, such as the mortgage and interest payment, HOA, management fees, ect.

Debt-to-income Ratio and FICO

Though these metrics are not unique to financing investment property, they will be taken into account when determining how much you qualify to borrow. Typically, lenders vacation rental financing requires higher credit scores than financing a home as a primary residence. Your lender can look at your financial position and create a clear mortgage plan for your situation uniquely.

Managing

Once you close on your new property you’ll have the option to manage yourself, or hire out a management company.

Obviously, managing your own property is not as easy for those who do not live nearby, compared to those who are local and live near their property. One popular way to have your property managed is by hiring a reputable management company, such as a local real estate office that specializes in property management.

Each management office operates differently, but typically a fee is collected from the homeowner based on how much rental money was collected that month

Owning vacation rental property in a high tourism area, such as Florida, is a major way to build wealth. For those considering stepping into owning vacation rental property, here’s a few things to consider.

]]>As college-bound students prepare for a new chapter, they are about to be faced with a multitude of decisions competing for their attention. But as they ease into their new life on campus, it's a time ripe with opportunity to lay down financial foundations that will serve them long after graduation.

Establishing excellent financial habits during college is the precursor to post-grad success. While conversations often revolve around savings and budgeting, there's one opportunity that is typically overlooked: purchasing a property in the college town. By converting the significant expense of rent during college into an investment, parents can pave the way for their child's future financial foundation. This strategic decision not only provides a tangible lesson in money management but can also become a launchpad to homeownership once they don their graduation caps.

The Advantage of Buying a Home in a College Town

Owning a home in a college town offers several benefits. The most obvious is this purchase can serve as an excellent investment opportunity. Since college towns tend to have a revolving influx of students, properties in college towns generally hold their value and appreciate over time.

In addition to having a place for the student to live while in college, theres also the opportunity to rent out extra rooms to college friends which can help cover the cost of the mortgage. On top of that, this could also familiarize students with landlord responsibilities, providing a valuable life lesson.

Finally, upon graduation, the student can sell the house and use the equity gained as a down payment for their next home. This would provide the student with a major head start in the competitive real estate market as they are entering their adulthood.

Financial Success Tips for College Students

Beyond purchasing a property, other strategies can set students up for financial success during their college years. Here’s some things for students to consider…

Credit Score Management: Learning the importance of and how to maintain a good credit score. One way to do this is by using a credit card responsibly and paying all bills on time. A good credit score will be invaluable when applying for loans or mortgages in the future.

Student Loan Management: Since a majority of students today take out student loans in order to pay for school, learning how to manage student loans well is essential. Always be sure to understand the terms of any student loans, including interest rates, grace periods, and repayment options. Students should keep track of their loan balance and make timely payments to avoid accruing unnecessary interest.

Savings and Budgeting: Even if it's a small amount, building the habit of saving money on a regular basis will be an invaluable lesson. Implementing a budget can help manage income from part-time jobs or allowances, which can help cover college expenses while still setting a little aside.

Avoiding Debt: When possible, avoid unnecessary debt. Credit cards should not be used for impulsive purchases but rather as tools for building credit history and for emergencies. Learning and practicing living within your means is a great habit to build while still in school.

We recommend chatting with a mortgage lender to understand the ins and outs of this unique investment approach, and how to get started. Remember, the goal isn't just to get through college; it's to be prepared for the financial responsibilities that come afterward. A little foresight now can lead to a robust financial future. Let's lay the groundwork today for the homeowners of tomorrow.

For many families, the quest for a dream home isn't just about granite countertops or a spacious backyard. The vicinity and quality of nearby schools play a monumental role in this decision-making process. As families prepare for the 'back to school' season, we diving into how schools impact home prices and what home buyers should take into consideration.

Balancing the Need for Quality Education and Affordable Housing

All parents want the best for their children, which likely includes a top-tier education. However, in some cases, homes in premium school districts come could with a premium price tag. For families on a budget, this presents a hurdle: should they stretch finances for a home in a top-ranked school district or prioritize affordable housing instead?

Talking with a mortgage lender can give you a better idea of the home price range for you to look at. By knowing this, you’ll be able to make more education decisions on which school districts to look in.

Consider the Logistics of Getting Kids to School and Work

Logistics is a major reason why a family may consider a move after the school year has already begun!

In many areas, kids don’t necessarily attend a school within close walking distance. Most families have some sort of commute to school. And in the case of living further out for more affordable housing, what impact and stress does that put on a family’s commute? On top of that, for working parents the proximity of schools to their workplace is just as crucial. A home might be close to a great school, but if it adds an hour to your work commute, the daily grind could become wearisome.

A good realtor can help you navigate looking at neighborhoods that meet your school and commute needs.

Cost of Property Taxes for Schools

Though it’s not always possible to predict how much property taxes will change over time, it is something to take into consideration when buying your next home. Higher property values often mean higher property taxes, and in most areas, these taxes fund local schools. Sometimes, what seems affordable at face value becomes less so when annual property taxes come into play.

How the Quality of a School Can Affect Home Value Over Time

Undoubtedly, a quality school can bolster property values in its district, making your investment in a home event more valuable. Homebuyers should research if their area is expected to expand their school district by upgrading current school, or adding new schools.

On the flip side, a school with challenges could mean trouble is on the horizon for your property value.

Needing to Change School Districts? Moving to the Area Could Be a Wise Move

Every home is districted for a specific school. If a parent, for any reason, wants to send their children to a different district, moving to that area may be the best choice.

In some places, like in Florida, parents can use school choice to enroll their child in a school outside of their district. Unfortunately, that could lead to a long waiting list. The best guarantee to get into that school is to take up residence locally.

A USDA loan is a type of home loan offered by the United States Department of Agriculture (USDA). It is designed to help low- to moderate-income individuals and families buy homes in areas designated as “rural”, particularly in areas where traditional financing may not be available.

One of the main benefits of a USDA loan is that it is 100 percent financing and does not require a down payment for a USDA loan, making it a great option for those who may not have a lot of savings or are unable to come up with a down payment for a traditional mortgage.

But, despite it’s name, the USDA loan isn’t just for buying property in the countryside. In fact, there’s many areas near urban areas that still qualify for the USDA loan.

According to USDA loan guidelines, areas that qualify are areas designated as “rural” according to the latest US Census. Thus, it is based on population of an area. But there are many towns and neighborhoods just outside of urban areas that meet the population qualifications. Or, there are rapidly developing areas that are becoming more urbanized, but haven’t yet been re-designated by the Census.

To see specific areas, check out the map here.

The bottom line is, if you’re looking for a 100 percent financing option, and think you may meet other USDA qualifications, the USDA loan is not one to overlook. Apply today to see if you qualify.

Before you decide to sell your house, it’s important to know what you can expect in the current housing market. One positive trend right now is homebuyers are adapting to today’s mortgage rates and getting used to them as the new normal.

To better understand what’s been happening with mortgage rates lately, the graph below shows the trend for the 30-year fixed mortgage rate from Freddie Mac since last October. As you can see, rates have been between 6% and 7% pretty consistently for the past nine months:

According to Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), mortgage rates play a significant role in buyer demand and, by extension, home sales. Yun highlights the positive impact of stable rates:

“Mortgage rates heavily influence the direction of home sales. Relatively steady rates have led to several consecutive months of consistent home sales.”

As a seller, hearing that home sales are consistent right now is good news. It means buyers are out there and actively purchasing homes. Here’s a bit more context on how mortgage rates have impacted demand recently.

When mortgage rates surged dramatically last year, escalating from roughly 3% to 7%, many potential buyers felt a bit of sticker shock and decided to hold off on their plans to purchase a home. However, as time has passed, that initial shock has worn off. Buyers have grown more accustomed to current mortgage rates and have accepted that the record-low rates of the last few years are behind us. As Doug Duncan, SVP and Chief Economist at Fannie Mae, says:

“. . . consumers are adapting to the idea that higher mortgage rates will likely stick around for the foreseeable future.”

In fact, a recent survey by Freddie Mac reveals 18% of respondents say they’re likely to buy a home in the next six months. That means nearly one out of every five people surveyed plan to buy in the near future. And that goes to show buyers are planning to be active in the months ahead.

Of course, mortgage rates aren’t the sole factor affecting buyer demand. No matter where mortgage rates stand, people will always have reasons to move, whether it’s for job relocation, changing households, or any other personal motivation. As a seller, you can feel confident there is a market for your house today. And that demand is pretty strong as buyers settle into where rates are right now.

Bottom Line

The way buyers perceive today’s mortgage rates is shifting – they’re getting used to the new normal. Steady rates are contributing to strong buyer demand and consistent home sales. Let’s connect so we can get your house on the market and in front of those buyers.

If you’re following mortgage rates because you know they impact your borrowing costs, you may be wondering what the future holds for them. Unfortunately, there’s no easy way to answer that question because mortgage rates are notoriously hard to forecast.

But, there’s one thing that’s historically a good indicator of what’ll happen with rates, and that’s the relationship between the 30-Year Mortgage Rate and the 10-Year Treasury Yield. Here’s a graph showing those two metrics since Freddie Mac started keeping mortgage rate records in 1972:

As the graph shows, historically, the average spread between the two over the last 50 years was 1.72 percentage points (also commonly referred to as 172 basis points). If you look at the trend line you can see when the Treasury Yield trends up, mortgage rates will usually respond. And, when the Yield drops, mortgage rates tend to follow. While they typically move in sync like this, the gap between the two has remained about 1.72 percentage points for quite some time. But, what’s crucial to notice is that spread is widening far beyond the norm lately (see graph below):

If you’re asking yourself: what’s pushing the spread beyond its typical average? It’s primarily because of uncertainty in the financial markets. Factors such as inflation, other economic drivers, and the policy and decisions from the Federal Reserve (The Fed) are all influencing mortgage rates and a widening spread.

Why Does This Matter for You?

This may feel overly technical and granular, but here’s why homebuyers like you should understand the spread. It means, based on the normal historical gap between the two, there’s room for mortgage rates to improve today.

And, experts think that’s what lies ahead as long as inflation continues to cool. As Odeta Kushi, Deputy Chief Economist at First American, explains:

“It’s reasonable to assume that the spread and, therefore, mortgage rates will retreat in the second half of the year if the Fed takes its foot off the monetary tightening pedal . . . However, it’s unlikely that the spread will return to its historical average of 170 basis points, as some risks are here to stay.”

Similarly, an article from Forbes says:

“Though housing market watchers expect mortgage rates to remain elevated amid ongoing economic uncertainty and the Federal Reserve’s rate-hiking war on inflation, they believe rates peaked last fall and will decline—to some degree—later this year, barring any unforeseen surprises.”

Bottom Line

If you’re either a first-time home buyer or a current homeowner thinking of moving into a home that better fits your current needs, keep on top of what’s happening with mortgage rates and what experts think will happen in the coming months.

Summer is in full swing in the Florida sun, and thousands of vacationers are taking advantage of the weather, beach, and endless things to do. But they aren’t the only ones enjoying this summer. Vacation rental property owners are also cashing in on the thriving tourism.

Owning vacation rental property in a high tourism area, such as Florida, is a major way to build wealth. For those considering stepping into owning vacation rental property, here’s a few things to consider.

Advantages

Long or short term

When buying property as a rental, homeowners have the option to choose long term or short term rentals. Both have pros and cons, but both are a great way to have your mortgage paid by someone else, and receive passive income.

Short term rentals are those geared towards tourists and vacationers. Typically, the property will be rented for a weekend or a week. The major advantage of this is more money is typically charged on a per night basis.

Long term rentals, such as 6 or 12 month leases, are typically geared towards locals or those who are moving to the area. The advantage of this is that your income coming in from the property is more predictable.

Florida also has an additional demand that is unique to our market, and that is “snowbird” or winter rentals. With these type of rentals, a person will rent a condo or house for 1 to 3 months during the winter season.

Building wealth

Buying investment property with the intent to rent out is a great way to build your net worth. Both long term rentals and short term rentals have pros

Your own vacation destination

Another major advantage to owning your own vacation rental property is that you and your family can vacation there whenever you want! Instead of paying money to stay at another’s property, you can visit your property that others are paying for.

Financing

When looking to finance your vacation rental property, your lender will factor in a few metrics unique to investment property management.

Debt Service Coverage Ratio

Lenders will take into account how much income the property is likely to produce. This is factored into your overall debt-to-income ratio, which we will cover below. The debt service coverage ratio measures how much rental income remains after paying for all costs, such as the mortgage and interest payment, HOA, management fees, ect.

Debt-to-income Ratio and FICO

Though these metrics are not unique to financing investment property, they will be taken into account when determining how much you qualify to borrow. Typically, lenders vacation rental financing requires higher credit scores than financing a home as a primary residence. Your lender can look at your financial position and create a clear mortgage plan for your situation uniquely.

Managing

Once you close on your new property you’ll have the option to manage yourself, or hire out a management company.

Obviously, managing your own property is not as easy for those who do not live nearby, compared to those who are local and live near their property. One popular way to have your property managed is by hiring a reputable management company, such as a local real estate office that specializes in property management.

Each management office operates differently, but typically a fee is collected from the homeowner based on how much rental money was collected that month

Owning vacation rental property in a high tourism area, such as Florida, is a major way to build wealth. For those considering stepping into owning vacation rental property, here’s a few things to consider.

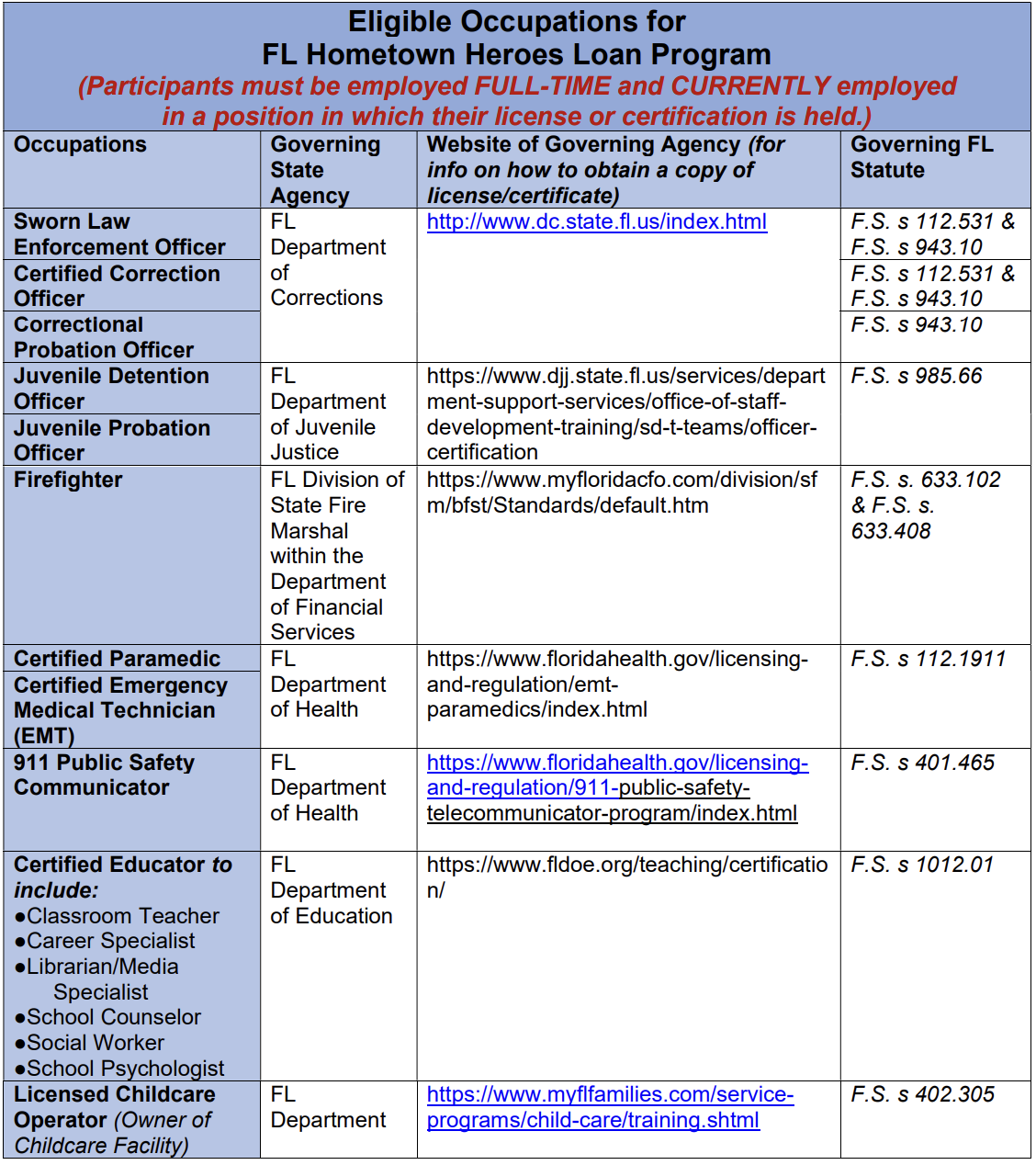

]]>As of July 1st, 2023, major changes have gone into effect to Florida’s very popular Hometown Heroes Program, thanks to a new bill passed by the Florida Legislature.

On March 29th, Governor Desantis signed Senate Bill 102, called the Live Local Act, which, among many other things, expanded the eligibility of the Florida Hometown Heroes down payment program.

Previously, the Florida Hometown Heroes Program was only available to people in certain professions, considered “front-line workers”. This included police officers, firefighters, certain medical professionals, among other professions. Now, it widens eligibility from career-based assistance to income-based assistance.

The program now offers down payment assistance in the form of a 0%, non-amortizing, 30-year deferred second mortgage. Which essentially means it is added to the back-end of a person’s mortgage. A person can receive up to 5% of the purchase price, capped at $35,000, to assist in the down payment and closing costs of the loan. Previously, the assistance was capped at $25,000.

To qualify for the program, borrowers must meet certain criteria. Loans are made available to persons or families whose household incomes do not exceed 150 percent of the state median income or local median income, whichever is greater. Borrowers must also be seeking to purchase a home as their primary residence, be first-time homebuyers and Florida residents, and employed full-time by a Florida-based employer. Documentation of full-time employment, or full-time status for self-employed individuals, of 35 hours or more per week is required. However, the requirement to be a first-time homebuyer does not apply to active duty service members of a branch of the armed forces or the Florida National Guard.

Additionally, the Florida General Assembly appropriated another $100 million towards funding the program.

The new changes to the Florida Hometown Hero Program is a significant step towards making homeownership more accessible for working Floridians. By reducing the barriers of down payment and closing costs, this program empowers individuals and families to attain long-term housing and financial security.

If you are a working Floridian aspiring to own a home, the Florida Hometown Hero Program may be the right opportunity for you. Contact our team today to learn more and take the first step towards realizing your dream of homeownership.

Join us for a FREE first-time homebuyer seminar July 22nd!

The home buying process can be overwhelming - we get it! That's why we're excited to host this education seminar with our very own Kayla Tarabay and Paul Cutler from The Riel Estate Team.

You don't have to go through the home buying process alone. Come learn about what you can do to prepare to buy your next home, downpayment assistance options, and so much more!

The home buying process can be overwhelming - we get it! That's why we're excited to host this education seminar with our very own Kayla Tarabay and Paul Cutler from The Riel Estate Team.

You don't have to go through the home buying process alone. Come learn about what you can do to prepare to buy your next home, downpayment assistance options, and so much more!

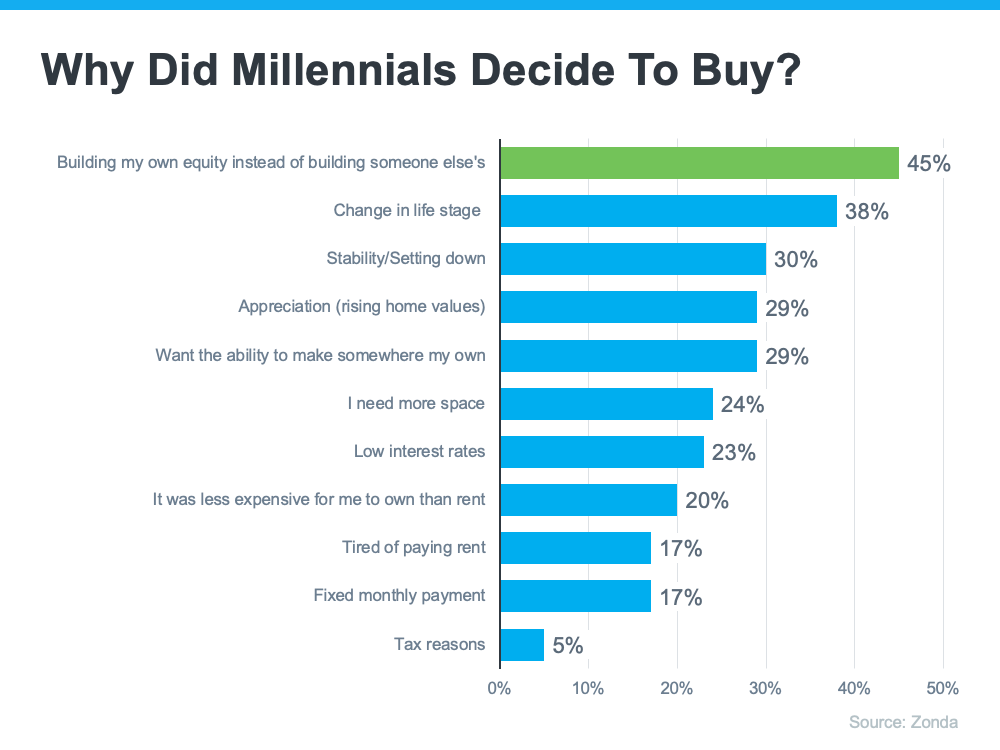

]]>In the United States, there are over 72 million millennials. If you’re part of that generation and have thought about buying a home, you aren’t alone. According to Zonda, 98% of millennials want to become a homeowner at some point if they aren’t already. But why? There are plenty of reasons you may choose to become a homeowner. Here’s why other millennials have made that decision (see graph below):

This graph shows why millennials are buying homes according to Zonda’s 6th annual millennial survey. The top reasons include building equity, a change in life stage, wanting stability, rising home values, and wanting to make somewhere truly their own. Here’s a look at each in more detail.

Building equity – Homeownership is a long-term investment that allows you to build wealth, increase your net worth, and become more financially stable. Beyond that, the alternative to owning a home is typically renting. With the way rents have risen so dramatically over time, it may make sense to build your own equity instead of the equity of the person you’re renting from.

A change in life stage – As a millennial, you’re reaching your prime homebuying years. That means you may be at the point where you need more space or a different location.

Stability or settling down – This could mean establishing your career or just generally deciding more concretely what you want your life to look and feel like. As that idea becomes clearer, you may want to establish that lifestyle in a particular place and put down roots.

Rising home values – By purchasing a home, you own an asset that traditionally increases in value over time. That can mean your home will have a higher resale value if you decide to move again.

Wanting to make somewhere “mine” – Owning a home gives a sense of freedom because you can customize it however you want, make updates as you see fit, and be yourself in a place that’s solely your own.

Bottom Line

There are plenty of great reasons why millennials are buying homes today. If you’ve thought about becoming a homeowner and any of these reasons resonate with you too, let’s connect to explore your options.